In the 1980s, credit cards became an American phenomenon. The once rarely-seen form of payment meandered its way into grocery stores, malls and the majority of the population’s daily life as they borrowed money for daily purchases. For up-and-coming entrants to the grown-up world, these minute pieces of plastic will likely cross the mind. Those looking for a fraud-protective, credit-building addition to their wallets will find that a well-selected credit card can serve a responsible user flawlessly. Under the age of 18, teenagers may become authorized users of their parents’ credit cards, but as students graduate into adulthood, their options expand.

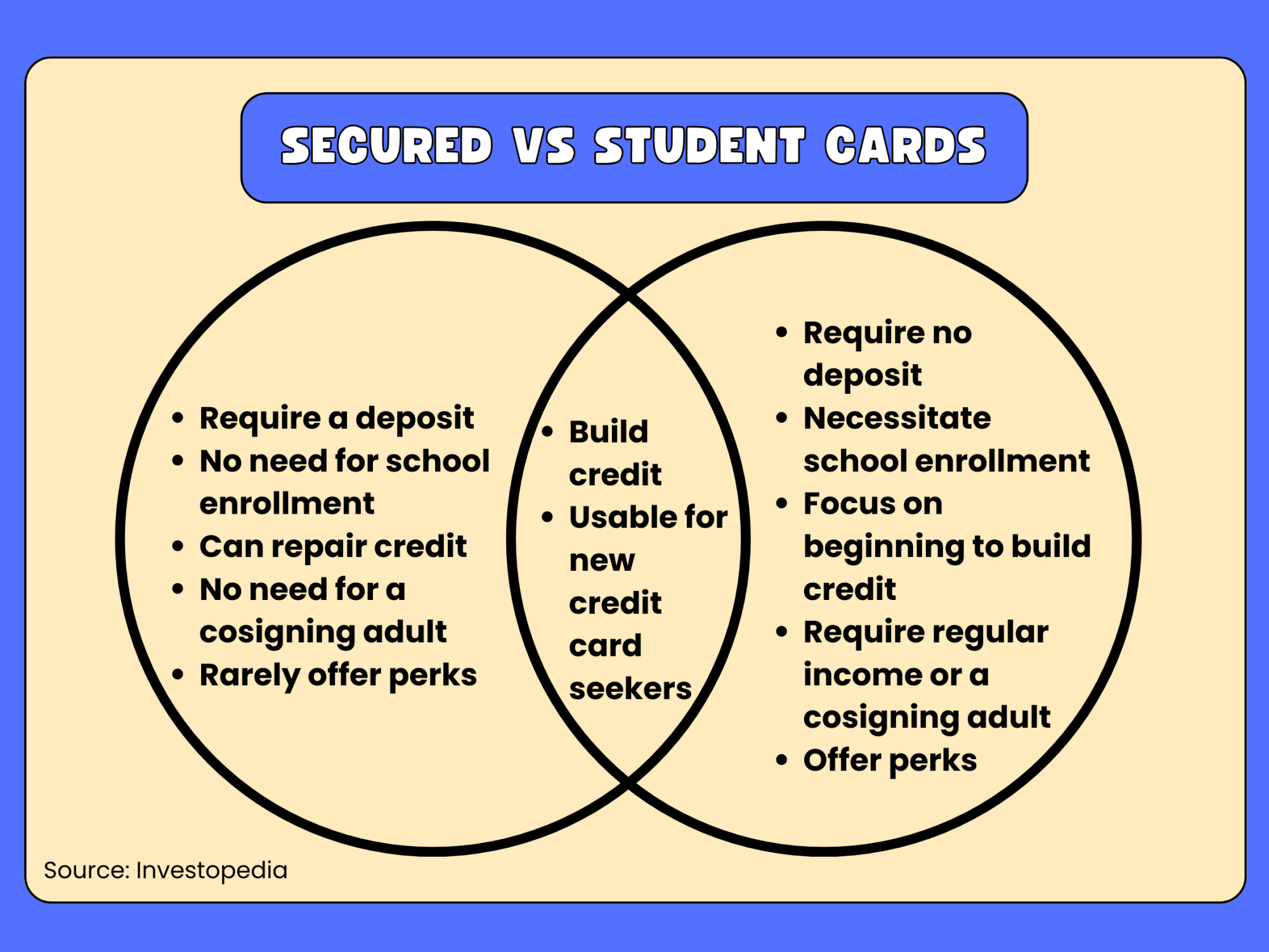

Typically, new credit card seekers will lack pre-existing credit history. This record, gained from paying bills on utilities, loans and credit cards, builds a score which could help people choose options with higher limits or lower interest rates. For inexperienced teenagers, the credit card options typically include secured cards, which require a deposit, or student cards with a similar premise, specifically for college kids. Alternatively, these people can create credit history with credit-builder loans, though these will create swaths of debt that will burden those unprepared to repay them. Essentially, the variability lies in the limit — the amount of money a person can charge to the card — and the interest — the extra debt accumulated as a charge for every month the card sits with the balance not paid off. Regardless, any bank’s credit cards will work similarly, and the real difference lies in how the person uses them.

With every swipe, credit cards offer the ability to improve or harm their owners’ credit scores. Cards include a minimum payment each month, which lenders will typically calculate as a minor percentage of the card’s balance. Generally, paying only the minimum payment will keep the person in debt, a risky situation to stay in. The deepest trouble a credit card holder could fall into, though, lies in failing to pay that bill, especially routinely, because that shows a lack of accountability, which will find its way onto the credit score.

“Monitor your spending so you’re not spending too much, and then pay as much off as you can the next month. They’re gonna tell you a minimum payment amount, but that minimum payment will essentially keep you in debt forever, so if you can pay more than the minimum, that’s the best way to stay out of long-term debt. Small purchases are probably better because it’s easier to pay it off. The big thing is, you need to be realistic in your purchases,” Advanced Placement (AP) Microeconomics teacher Tara Sisino said.

Credit cards promise their users control over their finances and a stronger credit history. Like any newfound control, this freedom poses risks. Still, any financially smart young person will find himself or herself with a powerful, credit-building piece of plastic in his or her wallet. This holds especially true considering the rewards, such as cash back, each might offer.